Market Notes - 22nd January

Fag-End buying pushed the markets higher while certain sectors saw bloodshed: Let's take a look on what drove the markets today

Indian stock markets staged a strong recovery on January 22, 2025, following a sharp decline the previous day. The BSE Sensex rose by over 570 points to trade above 76,100, while the Nifty50 gained 121.95 points to cross 23,100. This rebound was supported by positive global cues and investor focus on Q3 FY25 corporate earnings. Despite the recovery, market experts highlighted heightened volatility and recommended cautious trading strategies. The previous day's significant foreign investor selling of Rs 5,920 crore remains a point of concern for market participants.

NIFTY IT Index led the gains with megacap companies like TCS, Infosys, WIPRO and Tech Mahindra gaining more than 2.5%.

Sectors that become part of the bloodshed going for a few weeks now in the Indian Markets were:

EMS Companies: Even though the likes of Dixon Technologies reported decent Q3FY25 results, the expectations baked into the stock price were so high that the investors felt the Q3FY25 results to be mild and hence a massive de-rating going on the EMS companies since past few days. Dixon, Kaynes, Cyient touted to be multibaggers have shed over 10% in less than 4 trading sessions.

Solar companies like Waaree Energies and Solex Energy shed around 10% in a single trading session owing to the fear that Trump’s announced import tariffs will hurt Indian Solar Manufacturers.

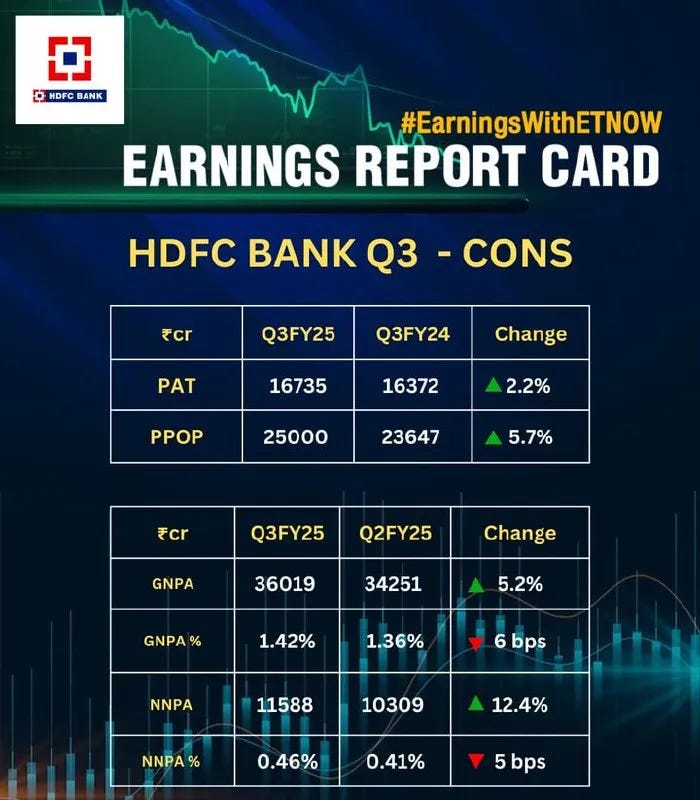

Results that Matter:

HDFC Bank reported a modest 2.2% year-on-year increase in net profit to ₹16,736 crore for Q3FY25, with net interest income growing by 8% to ₹30,653 crore. The bank's asset quality saw a marginal weakening, with gross non-performing assets rising to 1.42% of gross advances, while deposits grew by 15.9% year-on-year to ₹24,528 billion, outpacing the 3% growth in gross advances.

Hindustan Unilever Limited (HUL) reported a 19% year-on-year increase in net profit to Rs 3,001 crore for Q3 FY25, driven by a one-time exceptional gain of Rs 507 crore from the divestment of its Pureit business. The company's standalone revenue grew by 2% to Rs 15,195 crore, with the Home Care segment showing strong performance. Despite subdued FMCG demand trends, HUL maintained a healthy EBITDA margin of 23.5%. The company also announced the acquisition of premium beauty brand Minimalist and completed the divestment of its Pureit water purification business, positioning itself for long-term growth in the Indian FMCG sector.

Broader Developments:

The Indian government is expected to maintain the current capital gains tax structure for High Net Worth Individuals (HNIs) and individual taxpayers in the upcoming Budget 2025, providing a sense of relief to these groups. While some modifications to the Income Tax Act are anticipated, these changes are primarily focused on streamlining processes rather than implementing significant alterations to the existing tax framework. This approach suggests that the government is prioritizing simplification and ease of compliance over major structural reforms in the capital gains tax regime for the near future.

The Employees' Provident Fund Organisation (EPFO) reports in its latest "Provisional Payroll Data" that 14.63 lakh net members joined in November 2024—a 9.07% increase from October 2024. Year-over-year, net member additions grew by 4.88% compared to November 2023.

South Korea's consumer sentiment rose for the first time in three months this January. According to the Bank of Korea's survey, the consumer confidence index increased to 91.2 from December's 88.2.

To enhance the global competitiveness of India's diamond sector, the Department of Commerce has introduced the Diamond Imprest Authorization (DIA) Scheme. The scheme allows duty-free import of natural cut and polished diamonds under 1/4 carat (25 cents) while mandating a 10% value addition for export obligations.

The government has disbursed ₹1,596 crore under Production-Linked Incentive (PLI) schemes across six sectors, including electronics and pharmaceuticals, during April-September of this fiscal year. In 2021, the government launched PLI schemes for 14 sectors with an outlay of ₹1.97 lakh crore. These sectors include telecommunications, white goods, textiles, medical device manufacturing, automobiles, specialty steel, food products, high-efficiency solar PV modules, advanced chemistry cell batteries, drones, and pharmaceuticals. Of the total ₹1,596 crore disbursed, the PLI scheme for large-scale electronics manufacturing received the highest allocation at ₹964 crore.

Expert Talks:

Sandeep Tandon talks about three different phases in Indian markets that were dominated by three different kind of investors:

2003-2007 Bull Run: This period was entirely dominated by the FIIs who made exponential returns. The cycle peaked in Sept-Oct 2007 and then the global meltdown happened.

April 2009 Bull Run: During this bull run, HNIs made the most amount of returns. Maximum PMS and AIFs got established during this bull run to cater the HNIs. A lot of family offices got established during past 10 years, because a lot of businesses got sold and it became a norm to have your own family office. Sandeep believes that this trend peaked out around December 2017

April 2020 Bull Run: During the covid crash, all the rich folks who made money during the previous two cycles were worried. Broader retail public were not worried during the covid crash and have the mentality of buying the dips. These guys during the covid crash, sitting at home, with extra savings on hand due to reduced expenditure participated heavily in the bull run of past 4 years. Sandeep believes that the retail public led boom has a very large base considering the population of India and the financial penetration still being very low as compared to developed economies and also China. Hence, retail can be in the leadership position for at least another decade where they have the potential to dictate the direction of the markets with either direct investment into equities or via the route of SIPs.

As the market continues to navigate evolving dynamics, staying informed and adaptive remains essential. Whether it’s shifts in macroeconomic indicators, sector-specific trends, or key market events, each day offers new opportunities and challenges. Thank you for tuning in to today’s insights—let’s approach tomorrow with the same curiosity and resolve to uncover the stories driving the markets.